For Years, the Executive Committee has Blocked Real Reforms to Bring Increased Financial Transparency. Now, They Want to Codify Secrecy and Call It "Progress"

For Years, the Executive Committee has Blocked Real Reforms to Bring Increased Financial Transparency. Now, They Want to Codify Secrecy and Call It “Progress”

Calls for increased financial transparency in the Southern Baptist Convention are nearing a boiling point. Trust is crumbling, factions are hardening, and Cooperative Program giving is declining—5% below budget last month. Even designated giving is down 7% from this time last year.

The reasons for this decline are many, but at the root of it all is this one simple fact: Churches will not fund what they don’t trust.

There is ample evidence that SBC entities are losing the pre-eminent position they once had. We need transformative leadership to restore trust in the Southern Baptists’ Great Commission efforts. Instead, the SBC’s Executive Committee is doubling down on the financial opacity that is causing churches to lose confidence.

Last summer, the EC’s Committee on Convention Finances and Stewardship Development rejected my modest proposal for 990-level financial disclosure from our entities. My motion would require Southern Baptists to receive the same information other charities have to provide to the public; it would not require any filing with the government.

My motion is a simple step to bring our transparency up to today’s best practices. This might sound crazy, but it’s true: As it stands today, Planned Parenthood is more transparent than the SBC.

My motion was germane, appropriately made, in order, and deserved debate. That’s not what we got.

Instead, the EC refused to allow messengers to vote on it. Rather, they promised in their recommendation that the “Executive Committee, in cooperation and collaboration with SBC entities, institutions, and commissions, commits to reviewing the Business and Financial Plan, to determine ways to enhance transparency and clarity of reporting to the Convention, and will report its findings and recommendations to the messengers at the 2025 SBC Annual Meeting in Dallas, Texas.”

That phrase—“enhance transparency”—might sound like a step forward after a decade of messenger demands. But their new plan? It’s like enhancing pigs with lipstick. It’s a step backward, slashing the information churches and members can see. It presumes that Messengers didn’t “know” the current “transparency” model was working. That’s not the problem.

The real problem is that the current institutionalized efforts to be “transparent” fall woefully short of what Southern Baptists deserve and aren’t even followed to begin with.

The Executive Committee proposed an entirely new Business and Financial Plan that is less transparent than the current plan. The new proposal trades detail for efficiency and swaps concrete standards for vague ideals.

It shifts from a bottom-up, stakeholder-driven model—where churches hold their entities accountable—to a top-down, entity-first approach. It reinforces voluntary self-reporting rather than standards of disclosure.

In short, the new plan is a shift from Baptist congregationalism to Presbyterian elder rule, as applied to Convention governance.

The current plan isn’t perfect. Its transparency falls short of even secular nonprofit standards—something 990-level disclosure would fix. But the document we have now has some specific and detailed reporting.

The new plan muddies the waters even further. Here’s how.

Stripping Away Your Right to Know

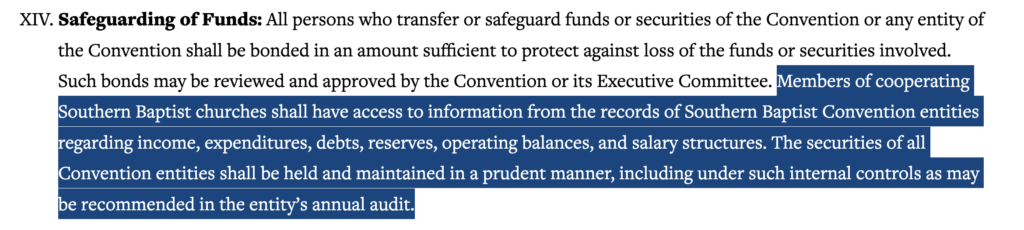

The current plan, in Article 14, guarantees SBC church members access to the entity’s records “regarding income, expenditures, debts, reserves, operating balances, and salary structures.” Here is the current language.

As it stands, this is like a member or shareholder’s right to inspect documents. In theory, this should give members (the churches of the SBC) a wide-open window to see detailed financial information of the entities.

In practice, it’s a fight—some entities dodge requests entirely, and others (like NAMB and IMB) describe “salary structure” processes rather than the information from entity records, thereby gaslighting requesters. When I sought this information as a test of how well the current system of “transparency” works, this was the response I got from the entities.

- SEBTS: First, they required the inquiring pastor to promise not to disclose the information to anyone else, and then they sent a salary scale that discloses the differing tiers of base salaries.

- SBTS: Sent a salary scale that gives the median base salary for each professional classification level.

- Gateway: Provided the salary scales for faculty, staff, and the president.

- NOBTS: Verified church membership via email with the church and then provided a salary scale, noting that the given upper and lower ends of faculty and administration “do not match current actuals.”

- MBTS: Did not respond to multiple requests from SBC pastors (a refusal to comply with Article 14 of the B&FP).

- SWBTS: Did not respond to multiple requests from SBC pastors (a refusal to comply with Article 14 of the B&FP).

- ERLC: Provided salary scales (base salary only) promptly but without qualification.

- NAMB: After multiple requests, they finally provided only their process for setting salaries (i.e., that the trustees set the salaries). Ultimately, this was a refusal to comply with Article 14 of the B&FP.

- IMB: After multiple requests, they also only provided their process for setting salaries (i.e., that the trustees set the salaries). They, too, refused to comply with Article 14 of the B&FP.

Keep in mind that this was just a request for the salary scales, which should have been promptly provided with actual numbers that show real compensation in the present.

Now, some people object to the 990-level disclosure because it requires disclosure of leadership compensation. Executive compensation disclosure isn’t about feeding discontent, as if keeping the salaries secret reduces complaints. This isn’t a morbid curiosity about what entity employees are making; this data provides essential benchmarks for evaluating how the trustees are performing their duties to hold these entities in trust.

Fundamentally, it’s about good governance, Christian governance. Such disclosure gives messengers a tool to evaluate the trustees they appoint. Executive compensation is one of the major decisions trustees make, and knowing a CEO’s pay forces trustees to justify it, aligning entity heads with the entity’s mission. The proposed plan omits that tool, shielding trustees from scrutiny and eroding accountability.

However, as you can see, many of our entities refuse to adhere to the “transparency” promised under the present iteration of the B&FP. This is exactly why I am working to secure increased financial transparency for SBC churches. Instead of heeding that call, the EC has proposed an amendment to make the obscurity currently practiced “official.”

Here’s the bottom line: The new plan doesn’t fix this; it codifies the evasion of the current rules. And it’s smuggled into what is essentially a rewrite of the entire governing document.

According to Baptist Press, “A rewritten Business and Financial Plan to be presented at the June Annual Meeting is designed to strengthen transparency and oversight for trustees who are approved to those positions by messengers, says Executive Committee President Jeff Iorg.” The document is shorter and updated, and on its face, there is nothing wrong with that.

However, the change to the “Disclosure” section is a major step backward in terms of real financial transparency. Here is the proposed change to the relevant section:

To be clear, if the new plan is adopted, messengers will lose all access to records and details. They will only have a right to staff’s “descriptions” of compensation processes—on request, filtered through confidentiality hoops. They will lose access to records on income, expenditures, debts, reserves, and operating balances.

In other words, again, this change codifies the current system’s failures. If adopted, churches (like mine) would not be able to rightfully claim that “the entities are noncompliant” because this amendment would sanction their obfuscation.

The Baptist Press article reports that, according to Dr. Iorg, “Recommending the new plan doesn’t set anything in stone.” He goes on to explicitly state that “If we discover deficiencies, the Business and Financial Plan can be amended until we feel it is adequate for its purpose.”

Well, Dr. Iorg, on behalf of many churches in the SBC, please hear me when I say the proposal is deficient from the start. Maybe you disagree. That’s okay. The Baptist way to solve this is to allow a full and free debate on the floor of the Convention this June in Dallas.

As it stands today, the Executive Committee appears intent on squashing that debate.

Reduced Disclosure?

The current plan mandates six specific disclosures in the Convention Annual: Statement of Financial Position, Statement of Activities, Statement of Cash Flows, a classified list of investments, receipts by state, and a board chair’s attestation of fiscal integrity.

The new plan does not mention these specific requirements. It does state that each entity’s audited financial statements will be published in their ministry reports and in the Convention Annual, but given that the entities currently play fast and loose with Business and Financial Plan language, the removal of specific requirements is a move away from concrete reporting standards.

Competition with the Cooperative Program?

As more churches withhold giving from the Cooperative Program due to the lack of financial transparency, the obscene levels of litigation spending, and mission drift, fund-raising rules also suffer. Entities now report detailed summaries—activity, goals, structure, costs, and results—for all fund-raising (except the Lottie Moon and Annie Armstrong offerings).

The new plan requires only broad-stroke reporting on “the total amount of contribution revenue received in the preceding fiscal year, along with combined categorized information about the sources of that revenue,” obscuring what’s raised, how, from where, and at what cost.

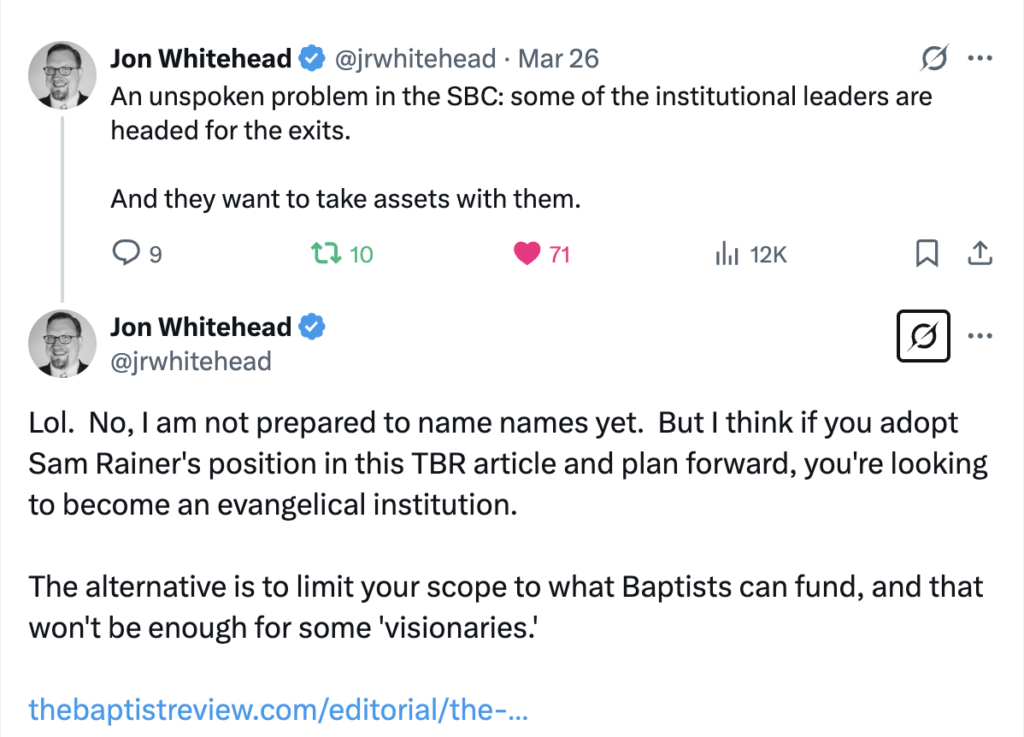

It also narrows the restrictions on soliciting churches to those “in friendly cooperation with the Convention.” Can entities now tap non-SBC churches for funding? Are our entities preparing for a post-Baptist, “general evangelical” future? Jon Whitehead seems to think so.

I think Jon’s warning should be heeded. That loophole invites outside influence. Outside funding creates the possibility of competition with the Cooperative Program, and that competition creates the conditions for mission drift.

For example, the ERLC received hundreds of thousands of dollars from liberal foundations, and its resulting work eroded trust so much that forty percent of messengers voted last year to abolish the commission altogether.

Of course, outside funding need not lead to CP competition and mission drift—it’s possible outside donors complement our cooperative mission. But how will churches and messengers know?

The plan states that “contributions will not be solicited or received that compromise the mission or reputation of the Convention or any Convention entity.” This clause improves upon the current plan but is still insufficient because outside funding would be disclosed neither to the Convention nor to the Executive Committee, as in the current scope of reporting.

Bloating Reserves?

The new plan also proposes a significant change to contingency reserves. The current plan requires entities to set both minimum and maximum reserves. Minimum reserves ensure entities have enough cash to pay their bills, and maximum reserves ensure they are deploying the missions dollars allotted to them to accomplish their assigned ministry tasks rather than stockpiling cash and assets.

Under the current plan, the maximum reserves are set by the entity and approved by the Convention. NAMB has faced criticism for allegedly bloating its reserves beyond what its bylaws allow. The new plan is silent on maximum reserve funds and removes the requirement of Convention approval.

“Trust Us” Isn’t Enough

The current Business and Financial Plan requires insufficient financial reporting to messengers and churches. But for all its flaws, where the current plan does require reporting, it does so with concrete, enforceable standards.

The EC’s proposed plan trades and the promise of hard facts for flowery institutional assurances. The new plan attempts to pacify messengers with the Accountability Letter: a board-signed promise of compliance on compensation, expenses, conflicts of interest, and fund-raising limits.

It’s a pat on the head, not a peek at the books.

Efficiency? Maybe. Transparency? Hardly.

The new plan provides little to no new information, instead just repackaging old information and even that in a less transparent manner. It’s lipstick on the same, ailing pig.

We might be Baptists, but we aren’t dumb. Don’t sell us a dog and claim it’s a racehorse.

Southern Baptists deserve better. The Cooperative Program thrives on trust, and building trust demands daylight. Therefore, Southern Baptists who care about restoring trust through transparency must come to Dallas prepared to demand new levels of transparency. Wise stewardship of missions dollars demands a greater accounting of them, not merely a repackaging of the old failures

The plan does not “enhance transparency”; it further obscures it, whispering, “Just trust us,” to the churches that foot the bills.

But that’s just the problem—we don’t.

Share This Story